Algorithmic Trading With ELIZE Versus High Frequency Trading(HFT)

Algorithmic Trading

Competition between investment firms is more intense than ever before as firms are expected to be able to beat the S&P 500 on a regular basis to retain and attract new investors. The market is evolving beyond previously established theories however investors still expect strong and consistent returns.

Traditional tools and fundamental analysis are no longer enough to stay competitive in the contemporary market. Investment firms need to stay one step ahead in order to be the first to recognize trends and take advantage of opportunities. To stay competitive they are looking to employ the most advanced tools to enhance performance. Algorithmic trading is now a growing trend filling this void. Algorithmic “Buy” and “Sell” orders account for 60%-70% of the US equity market volume. Previously, only large investment firms and hedge funds were able to utilize these advanced mathematical models but ELIZE: Daily Market Forecast, a financial start-up, has developed an advanced self-learning algorithm that is being employed by professionals and retail investors alike.

There are however, two types of algorithmic trading that are very distinguishable. The first is high frequency trading (HFT). The advantage of this form of algotrading is to be quicker than the rest of the market, but it only can be utilized by a select group of traders and there are extensive consequences that affect the entire market. The system is not “smart” or provides any real valuable insight for investors as it only blindly follows short-term trends. This form of algotrading is also publically ethically debated. The second form of algotrading, utilized by the ELIZE self-learning algorithm is called quantitative trading. This form provides valuable market insight to retail and professional trader alike that is used in conjunction with traditional forms of analysis. Algorithmic traders benefit from this “second opinion” in their decision making process by verifying their own analysis or discovering new market opportunities while still maintaining complete control of their portfolio. This article will delineate and clarify the disparities between these different forms of algorithmic trading.

High Frequency Trading (HFT)

The main goal of High Frequency trading is to extract a lot of small returns gained in very short period of time that do the actual trading for investment firms with real time intelligence and can trade in milliseconds. HFT technological costs are enormous and there is high competition amongst firms. Typically an HFT operates online using real-time data about transactions utilizing tremendous amounts of data in real time. In order to extract these small returns, the algorithm must be able to execute very quickly, which claims high demand on CPU performance (central processor unit) and memory handling. The algorithm then must minimize the amount of data used for decision-making. The most common type of algorithm used is called “one-pass.” As the title suggests, this algorithm reads each new piece of information only once and then tosses it away. Such algorithms usually operate with aggregated data dating back to five minutes of history to create a one-minute projection into the future. Based on this projection the algorithm makes decision on quotes and trades.

As competition is increasing with HFT, performance of each HFT algorithm becomes more decisive in the effectiveness of the system. This performance is highly dependent on infrastructure, representing a large proportion of expenses related to High Frequency Trading. Literally every meter of cable matters and the algorithm may lose its advantage of speed in any moment, significantly threatening the ability to make a profit.

The reason speed is imperative is that HFT works by placing and quickly canceling orders to find the price buyers and sellers are ready to trade at. This price-volume information is used to recognize developing trends. At the end of the day, they liquidate positions. Since these algorithms are so effective at moving capital, they have become quite controversial because retail investors are not able to compete. These algorithms can simultaneously process volumes of information at a rate no human can process, giving investment firms a huge advantage. This allows HFT traders to have the first choice in trades, a form of scalping. All in all, these algorithms add an extra element of volatility and have been at least partially responsible for market crashes in the past. In a crisis, these HFT algorithms liquidate positions in seconds, causing huge imbalances and price swings.

This risk is currently present. One notable example is the May 6, 2010 Flash Crash. As the US stocks traded down most of the day due to the debt crisis in Greece, the market dropped 600 points at 2:42 pm, on top of the 300 points it was already down for an almost 1000 point loss for the day. By 3:07 pm the market regained most of the 600-point drop back. Even though the algorithms were able to correct most of the damage the flash crash left a scar on the market. In the 17 of the 25 months since then investors have withdrawn a net $137 billion out of the U.S. stock market according to Lipper. Since a level field is needed to give everyone an equal chance, several European countries and Canada are curtailing or banning HFT due to concerns about volatility and fairness.

Quantitative Trading

The second form of algorithmic trading is known as quantitative trading or longer term trading. These algorithms analyze the structure and the trends in the market, find predictable patterns, and investors trade upon these machine-derived forecasts. This form of trading is very suitable for most investors, retail or professional. The ELIZE predictive algorithm belongs to the second form of algorithmic trading.

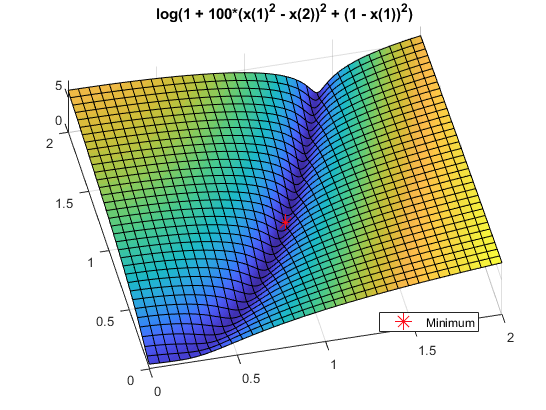

While we cannot speak on every algorithm meant to predict the market, the ELIZE market prediction system is based on artificial intelligence (AI), machine learning (ML), as well as utilizes elements of artificial neural networks and chaos theory. Machine learning provides an innate acumen to our comprehension of market dynamics and behavior. The algorithm has a built-in general mathematical framework that generates and verifies statistical hypotheses about stock price development. Machine learning tools such as artificial neural networks make this prediction system self-learning, and consistently determined to become more precise. This framework is used to generate initial testing models over a test sample of data. The goal of this phase is to validate the accuracy of the algorithm as well as to fine-tune the fitness function, which represents the actual goal of the algorithm expressed as a mathematical function. When the algorithm finds the global minimum of the fitness function attached to one of the models generated, it fulfills its goal.

From the mathematical perspective finding a global minimum is a very complex task and bears a risk of finding a local minimum, which seems to be global from the perspective of surroundings of the point but there can be found points less than that one. The situation is illustrated in the figure above. To increase the chance of finding the global minimum, we need to combine multiple searching procedures. When the algorithm proves its ability to generate valid results over the sample data, we can then use it to real data analysis. Every run the algorithm improves its predictive ability, as it generates new models and verifies them to the fitness function, therefore providing better and better results.

Algorithmic Trading With The ELIZE Market Prediction System

Many investors hear about algorithmic trading in the news but are not sure how they can use algorithms to their advantage. There are many successful strategies that can be easily applied with the ELIZE algorithm that are discussed in detail here. In general however, algorithms can help protect investors from human factors such as their own biases, psychological pressures, the omnipresent market risk, and fluctuating volatility.

The ELIZE algorithm has two indicators that guide investors to making better financial decisions. The first indicator is the signal, which gives the direction and the relative “scale” of the predicted movement of an asset, while also giving the level of confidence the algorithm has for that prediction, called the predictably indicator. This indicator is based on the past performance of the corresponding predictor. Both of these parameters are important and as a general rule, regardless of the type of forecast, the higher both are the better. It is recommended to consider both the signal strength and predictability.

Investors stand to benefit from using the ELIZE advanced algorithmic system because algotrading allows for objective valuation of assets, quantitative forecasts of the future trends for six different time horizons at a very low expense to receive daily predictions. Plus investors can have the option to get up to twenty top recommendations of stocks, currencies, ETF’s, commodities, world indices and even customized predictions that can be added with any forecast. Utilizing the immense amount of selections available, an investor can design a well-diversified portfolio that has scalable predictions to support each decision for every component.

Algorithms play a role in virtually every technology we have contact with including our favorite mobile applications, to search engines and social media networks that we use daily. So it is natural that we as investors in this hi-tech world utilize algorithms to help us invest better. Even in the 21st century, some are skeptical about whether or not an algorithm can really make a difference in a portfolios return. These results are constantly improving as the algorithm learns from its successes and failures. However in the skeptic’s defense, not all algorithms are created equally but the ELIZE self-learning algorithm is unique and cannot be whipped up by published formulas.

The market prediction system works by tracking the flow of money from one market or investment channel to another. On a daily basis new data is added to our fifteen-year historical file.

Then a learning and prediction cycle is run with the new data included. The algorithm subsequently produces predictions for over 10,000 assets with six time horizons for each. It separates the predictable part from stochastic (random) noise and then creates a model that projects the future trajectory of the given market in the multi-dimensional space of other markets. The algorithm outputs the predicted trend as a number, which in turn, is used by traders to identify when to enter and exit the market. While the algorithm can be used for intra-day trading, the predictability tends to become stronger over longer time-horizons such as the 1-month, 3-month and 1-year forecasts.